View:

FOMC Still Waiting For Data to Justify Easing

May 1, 2024 7:58 PM UTC

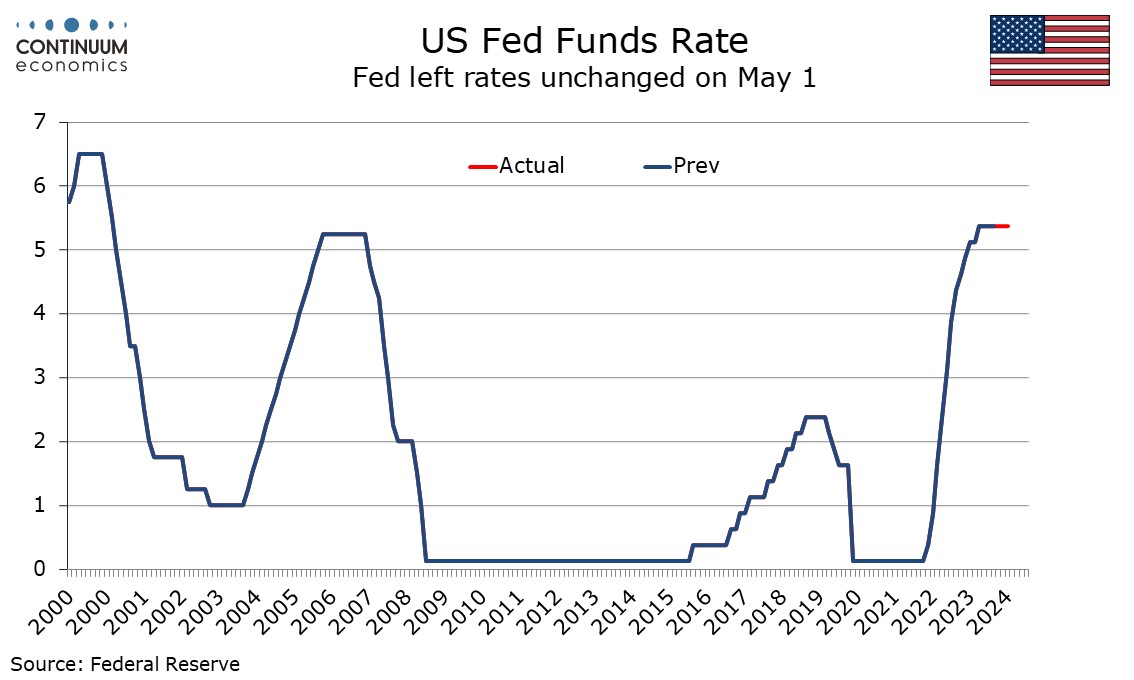

The May 1 FOMC statement, and Chairman Jerome Powell’s press conference, while noting recent inflation disappointment, did not deliver a strong pivot in tone. The Fed is still waiting for data to allow easing to take place, but still expects inflation to slow, and looks ready to respond once data

Markets: Fed Rather Than Middle East Worries

April 17, 2024 12:34 PM UTC

Global markets are being driven by a scale back in Fed easing expectations and we see a 5-10% U.S. equity market correction being underway. However, with the market now only discounting one 25bps Fed cut in 2024, any downside surprises on U.S. growth or better controlled monthly inflation numbers

Asia Open - Overnight Highlights

May 17, 2024 12:00 AM UTC

EMERGING ASIA

EM currencies perform individually against the USD as the greenback followed the post CPI drop initially before rebounding in the New York session. KRW saw the largest gains of 1.79%, followed by THB 1.09%, IDR 0.65%, TWD 0.61%, MYR 0.5%, PHP 0.12% and HKD 0.11%; the biggest losers are

U.S. April Industrial Production - Underlying picture looks flat

May 16, 2024 1:31 PM UTC

April industrial production was unchanged with a downward revision to March offset by an upward revision to February. Manufacturing was weak at -0.3% though outside a negative correction in autos the drop was only 0.1%, leaving a fairly flat underlying picture.

Brazil: Possible Impacts of the Floods

May 16, 2024 1:07 PM UTC

Unprecedented floods in Rio Grande do Sul, a state that contributes 6.4% to Brazil's GDP and 13.3% to its agricultural production, have submerged several cities. The immediate halt in economic activity may reduce Brazil's Q2 GDP by up to 0.4%. The federal government is increasing aid, potentially ra

U.S. Initial Claims, Housing Starts, Philly Fed - No real surprises but consistent with a modest slowing

May 16, 2024 1:00 PM UTC

The latest data is all close to consensus, initial claims partially correcting a sharp rise last week, housing starts correcting a sharp fall last month but permits seeing a second straight dip while the Philly Fed corrected from a strong preceding month but remains positive. All this is consisten

France and Japan: Debt Fuelled Growth Problem

May 16, 2024 10:30 AM UTC

Most of the surge in debt/GDP in Japan and 40% in France is due to higher government debt and this should not be a binding constraint provided that large scale QT is avoided – we see the ECB slowing QT in 2025 and are skeptical about BOJ QT in the next few years. The adverse impact of higher deb